Stacked vs. Non-Stacked Car Insurance in 2026 [Differences Explained]

When comparing stacked vs. non-stacked car insurance, USAA set the least expensive non-stacked coverage at $105 per month and stacked at $120 per month. Stacked insurance limits coverage for two or more automobiles together, and non-stacked sets the limits individually for each vehicle.

Read more

Find the Lowest Car Insurance Rates Today

Quote’s drivers have found rates as low as $42/month in the last few days!

Table of Contents

Table of Contents

Feature Writer

Chris Tepedino is a feature writer that has written extensively about car insurance for numerous websites. He has a college degree in communication from the University of Tennessee and has experience reporting, researching investigative pieces, and crafting detailed, data-driven features. His works have been featured on CB Blog Nation, Healing Law, WIBW Kansas, and Cinncinati.com. He has been a...

Chris Tepedino

Insurance Claims Support & Sr. Adjuster

Kalyn grew up in an insurance family with a grandfather, aunt, and uncle leading successful careers as insurance agents. She soon found she has similar interests and followed in their footsteps. After spending about ten years working in the insurance industry as both an appraiser dispatcher and a senior property claims adjuster, she decided to combine her years of insurance experience with another...

Kalyn Johnson

Updated April 2025

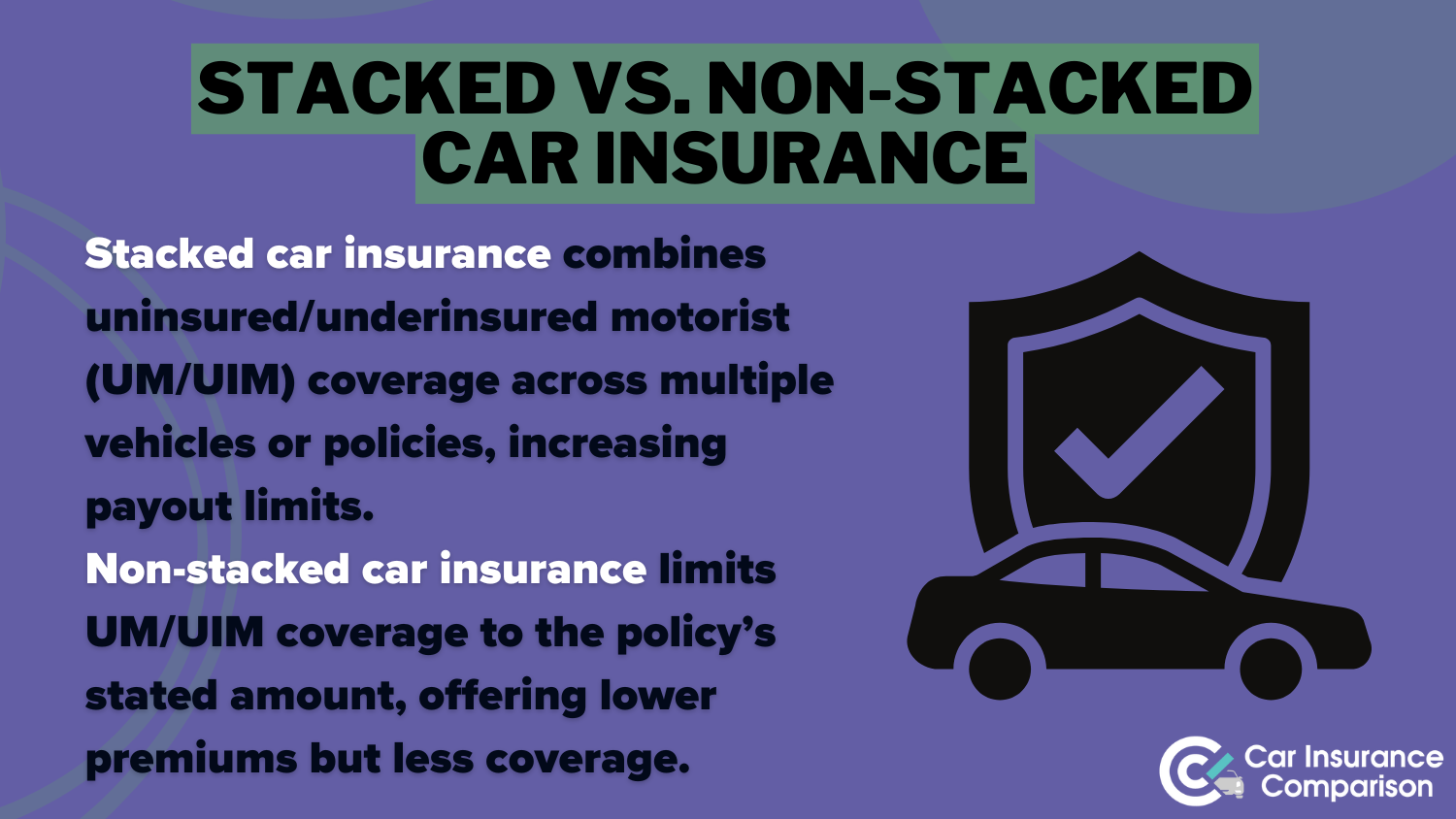

What are stacked car insurance and non-stacked insurance? What are stacked car insurance and non-stacked insurance? It lets you stack uninsured/underinsured motorist coverage on more than one car, raising your payout limits. While it provides superior protection, it will cost you more in premiums.

Non-stacked insurance maintains the coverage independently for every car, capping payments but being less expensive. To be economical, USAA is the lowest at $105 for non-stacked and $120 for stacked insurance.

- Non-stacked insurance has separate limits per vehicle

- Stacked insurance combines coverage limits for multiple vehicles

- Stacked insurance is pricier but provides greater protection

To make the best choice, compare the cheapest car insurance companies to find the right balance between cost and coverage. Understanding stacked vs. non-stacked insurance ensures you get the protection that fits your needs. See how much you’ll pay for car insurance by entering your ZIP code into our free comparison tool.

Stacked vs. Non-Stacked Car Insurance

In answering the question, “What’s the difference between stacked and unstacked insurance?” it’s a matter of how uninsured motorist coverage limits are used for multiple vehicles. Stacking car insurance lets you combine coverage from different cars to get a bigger payout if you’re in an accident.

For example, if you have two cars with $100,000 in uninsured motorist property damage coverage each, stacking vs. non-stacking means you’d have $200,000 in total coverage instead of being limited to $100,000 per vehicle.

Stacked coverage ensures higher combined limits apply, protecting you across all family vehicles.

Brad Larson LICENSED INSURANCE AGENT

While stacked insurance has higher premiums, it can prevent large out-of-pocket costs in a severe accident with an uninsured driver. Non-stacked insurance has lower rates but limits coverage to each vehicle’s individual policy amount.

Free Insurance Comparison

Compare Quotes From Top Companies and Save

Non-Stacked vs. Stacked Car Insurance Rates

Stacked insurance availability varies by state and insurance provider. Some states allow stacked car insurance on a single policy covering multiple vehicles, while others only permit stacking across separate policies for each car. Certain states do not allow stacking at all.

Stacked vs. Non-Stacked Car Insurance Monthly Rates by Provider & State Availability

| Insurance Company | Non-Stacked Coverage | Stacked Coverage | States Available |

|---|---|---|---|

| $120 | $140 | All states | |

| $115 | $135 | Selected States | |

| $128 | $148 | All states | |

| $110 | $125 | All states | |

| $130 | $150 | All states | |

| $125 | $145 | All states | |

| $127 | $147 | All states | |

| $118 | $138 | All states | |

| $122 | $142 | Selected States | |

| $105 | $120 | All states |

Even if your state permits stacking or non-stacking insurance coverage, not all insurance companies offer it. If your current provider does not allow stacked car insurance, you may need to explore other insurers that do.

Read More: Compare Car Insurance by Coverage Type

Check with your state insurance department or company to determine if uninsured motorist property damage coverage can be stacked in your state.

Stacking vs. Non-Stacking Insurance Coverage Levels & Benefits

With stacking or non-stacking insurance, coverage limits are determined by your policy structure. Stacking lets you add uninsured motorist coverage to multiple vehicles, giving you extra protection. For example, if you have two cars with $50,000 in coverage each, stacking increases your total limit to $100,000.

Compare the key differences between stacked and non-stacked car insurance to determine the best option for your needs.

Key Differences Between Stacked and Non-Stacked Coverage

Feature Stacked Coverage Non-Stacked Coverage

Coverage Limits Combines limits from multiple vehicles Limited to one vehicle's policy

Cost More expensive Cheaper

Availability Only in certain states Available in all states

Best for Multi-car policyholders Single-car owners or budget-conscious drivers

Non-stacked insurance, on the other hand, maintains the coverage distinct, and each car’s limit applies separately. So, if an accident costs $75,000 but your car’s coverage is only $50,000, you must pay the $25,000 difference out of pocket. Some states allow stacking, while others prohibit it. If stacking isn’t available, single-limit car insurance may offer higher protection under one cap.

Stacked vs. Non-Stacked Insurance: Choosing the Right Coverage

When choosing between stacked and non-stacked coverage, your risk tolerance, the number of vehicles you have, and your financial status are factors you should consider.

Even though stacked coverage is likely to cost more, the broad coverage it offers in extreme situations might be worth it. If your state and insurance provider allow it, you might want to consider combining your car insurance for multiple vehicles.

Non-stacked insurance is generally cheaper each month, but if you’re involved in a serious accident with an uninsured driver, you could end up facing substantial out-of-pocket expenses. On the other hand, stacked coverage allows you to combine the insurance limits for all your vehicles, potentially saving you a significant amount in the event of a major accident.

Read More: USAA Car Insurance Review

Based on the rates provided, the cheapest non-stacked coverage is available from USAA at $105 per month, while the most affordable stacked coverage is also from the same company at $120 per month.

These lower rates could make comprehensive protection more accessible while maintaining your budget. See how much you’ll pay for car insurance by entering your ZIP code into our free comparison tool.

Frequently Asked Questions

Is stacked insurance worth it?

Stacked insurance is worth it for multi-vehicle households in high-risk areas, as the increased protection from combining car insurance coverage limits offers significant financial security despite the slightly higher monthly premiums.

What is the difference between stacked vs. non-unstacked insurance?

Stacked insurance allows you to combine uninsured/underinsured motorist coverage limits from multiple vehicles, while non-stacked insurance keeps each vehicle’s coverage separate, offering less protection but at a lower premium.

What does non-stacked mean in auto insurance?

Non-stacked means your coverage limits apply separately to each vehicle and cannot be combined. If your coverage limit is $50,000 per vehicle, you cannot access more than that amount per claim. See how much you’ll pay for car insurance by entering your ZIP code into our free comparison tool.

Do you need stacked auto insurance if you have one car?

No, stacked insurance only benefits policyholders with multiple vehicles. With one car, there’s nothing to “stack,” so you should opt for non-stacked coverage or higher individual limits.

What are the cost differences between stacked and non-stacked coverage?

Stacked coverage typically costs 15-20% more than non-stacked options. For example, USAA offers non-stacked coverage at $105 monthly and stacked at $120, making it the most affordable option.

How does uninsured motorist non-stacked coverage work?

Uninsured motorist non-stacked coverage limits your payout to the maximum coverage amount for the specific vehicle involved in the accident, regardless of how many vehicles you have insured.

Read More: Uninsured and Underinsured Motorist Coverage (UM/UIM

What is rejecting stacked limits of uninsured motorist coverage?

Rejecting stacked limits means you’re choosing not to combine uninsured motorist coverage across vehicles, which lowers your premium but limits your protection to each vehicle’s individual policy amount. Enter your ZIP code into our free comparison tool to see how much car insurance costs in your area.

How does stacked vs. unstacked insurance in Florida work?

Florida allows coverage for both stacked and non-stacked uninsured motorists. Stacking in Florida can be vertical (combining limits within one policy) or horizontal (combining across separate policies), providing flexible options for residents.

What is non-stacked uninsured motorist coverage?

Non-stacked uninsured motorist coverage limits your protection to the policy amount of the vehicle involved in the car accident, preventing you from combining coverage limits across multiple vehicles on your policy.

Which insurance companies offer the best rates for stacked and non-stacked coverage?

USAA offers the lowest rates for both options: $105 a month for non-stacked and $120 a month for stacked coverage. Geico follows with $110 a month for non-stacked and $125 a month for stacked insurance.

Related Articles

-

Oct 2024

Compare SSI Recipient Car Insurance Rates [2026]

-

Sep 2024

Do I have to report a car accident to my insurance company or the police?

-

Feb 2025

Can you pay your car insurance yearly?

-

Oct 2024

Online Car Insurance Quotes Without Personal Information

-

May 2026

10 Best Usage-Based Car Insurance Companies [2026]

Get a FREE Quote in Minutes

Insurance rates change constantly — we help you stay ahead by making it easy to compare top options and save.